Factoring is a type of finance where a business sells its accounts receivable to meet short-term liquidity needs, with the factor paying the amount due minus fees. There are four types of factoring: recourse and non-recourse factoring, domestic and export factoring, disclosed and undisclosed factoring, and advance and maturity factoring.

Recourse factoring requires the company to buy back any unpaid invoices, while non-recourse factoring shifts the risk to the factoring company. Domestic factoring focuses on invoices within a country, while export factoring involves international invoices. Disclosed factoring is transparent to customers, while undisclosed factoring is not.

Lastly, advance factoring provides immediate funds, while maturity factoring releases funds at a later date. Overall, factoring allows businesses to improve cash flow by selling their accounts receivable.

Credit: www.gophermods.com

Introduction To Factoring

Factoring is a type of finance where a business sells its accounts receivable to a third party for short-term liquidity. There are different types of factoring, including recourse and non-recourse factoring, domestic and export factoring, and disclosed and undisclosed factoring.

Definition Of Factoring

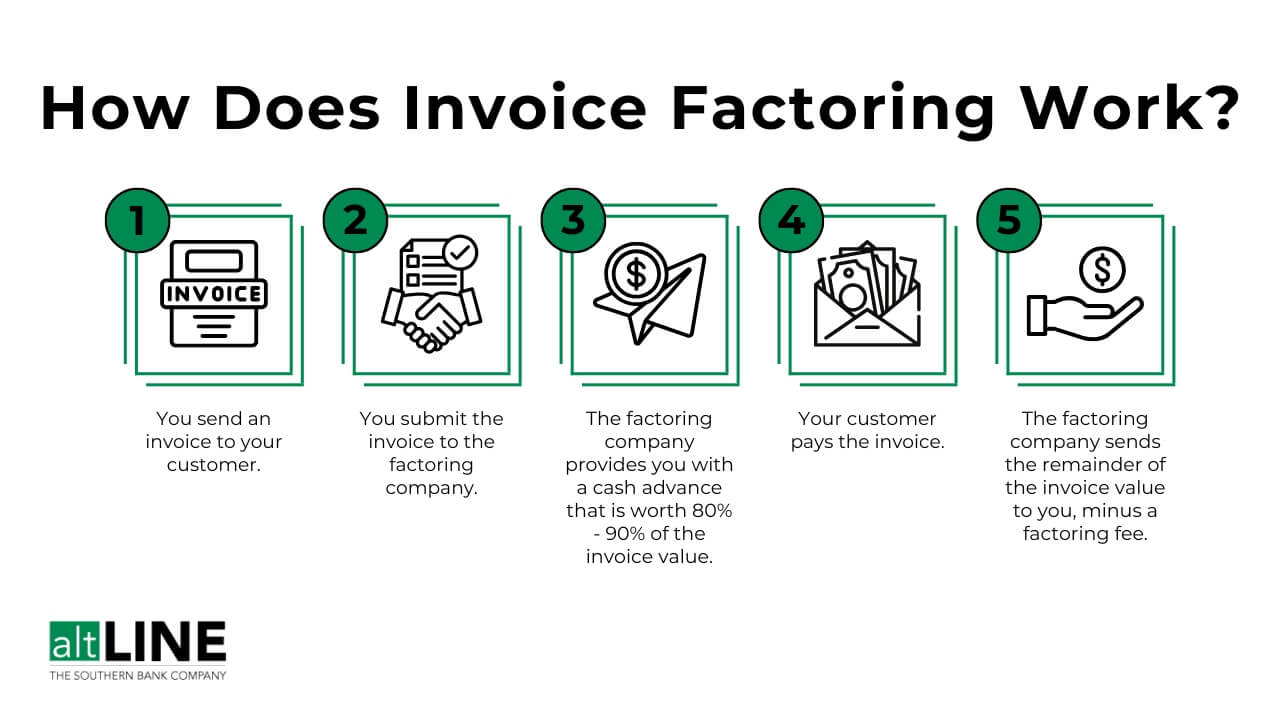

Factoring is a type of finance in which a business sells its accounts receivable, also known as invoices, to a third party. This is done in order to meet the business’s short-term liquidity needs. In this transaction, the third party, known as the factor, pays the business the amount due on the invoices, minus its commission or fees.Benefits Of Factoring

Factoring offers several benefits for businesses looking to improve their cash flow. Here are some of the advantages of factoring:- Improved Cash Flow: By selling their invoices to a factor, businesses can receive immediate payment instead of waiting for their customers to settle their invoices. This helps businesses maintain a steady cash flow and meet their financial obligations.

- Debt-Free Financing: Factoring allows businesses to access funds without taking on additional debt. Unlike traditional loans, which require collateral or a strong credit history, factoring is based on the value of the invoices. This makes it an attractive financing option for businesses with limited credit history or a high risk profile.

- Outsourcing Accounts Receivable: When a business engages in factoring, it transfers the responsibility of collecting payment from customers to the factor. This frees up valuable time and resources for the business, allowing them to focus on their core operations.

- Credit Risk Mitigation: Factors often conduct credit checks on customers before purchasing invoices. This helps businesses minimize the risk of non-payment by identifying customers with a history of late or non-payment. Additionally, in non-recourse factoring, the factor assumes most of the risk of non-payment.

Types Of Factoring

Factoring is a versatile financing option for businesses seeking to improve their cash flow. There are various types of factoring available, each with its own unique features and benefits. Understanding these different types can help you choose the most suitable option for your business needs. Here, we will explore four common types of factoring:

1. Recourse Factoring

Recourse factoring is the most commonly used type of factoring. In this arrangement, the factor purchases the accounts receivable from the business but holds the right to recourse back to the business if the customer fails to pay. In other words, if the customer does not pay within the agreed period, the business is responsible for buying back the invoice from the factor.

This type of factoring provides businesses with quick access to cash and is suitable for those who are confident in their customers’ payment ability. It is generally less expensive compared to non-recourse factoring because the business assumes the risk of any non-payment.

2. Non-recourse Factoring

Non-recourse factoring is the opposite of recourse factoring. In this arrangement, the factor assumes most of the risk of non-payment by the customers. If a customer fails to pay, the factoring company absorbs the loss.

While this type of factoring offers greater protection to the business, it tends to be more expensive than recourse factoring due to the higher risk borne by the factor. Non-recourse factoring is suitable for businesses with customers who have a higher default risk or those who prefer not to assume the risk themselves.

3. Domestic Factoring

Domestic factoring involves the purchase of accounts receivable from domestic customers only. It is a common choice for businesses that primarily operate within their own country. The factor works closely with the business to manage invoicing, collections, and credit checks.

This type of factoring provides businesses with the advantage of local expertise and knowledge in dealing with their domestic customers. It streamlines the collection process, allowing businesses to receive cash quickly and reduce the administrative burden associated with managing receivables.

4. Export Factoring

Export factoring, on the other hand, involves the purchase of accounts receivable from international customers. It is a suitable option for businesses that engage in cross-border trade. Factors specializing in export factoring possess the necessary expertise to manage the complexities of international transactions, including credit checks, currency exchange, and language barriers.

Export factoring provides businesses with a reliable cash flow solution while mitigating the risks associated with international trade. It helps businesses expand their customer base and enter new markets with confidence.

In conclusion, understanding the different types of factoring allows businesses to choose the option that best aligns with their specific needs. Whether it’s recourse or non-recourse, domestic or export, factoring can provide businesses with the much-needed cash flow to fuel their growth and success.

Understanding Recourse Factoring

Recourse factoring and non-recourse factoring are two types of invoice factoring, with recourse factoring being more common. In recourse factoring, the business is responsible for buying back any invoices that the factoring company is unable to collect payment on, while in non-recourse factoring, the factoring company assumes most of the risk of non-payment by customers.

Definition Of Recourse Factoring

Recourse factoring is a type of invoice factoring in which the seller retains the responsibility for any invoices that remain unpaid by the buyer. In other words, if the buyer fails to pay the invoice, the seller will be required to repurchase the invoice from the factor.Responsibilities And Risks For The Seller

When opting for recourse factoring, the seller assumes certain responsibilities and risks. Here are some key points to consider:- The seller is responsible for the creditworthiness of the buyer. If the buyer defaults on payment, the seller must reimburse the factor.

- The seller is responsible for any legal actions required to collect outstanding payments from the buyer.

- There is a higher level of risk involved for the seller, as they are ultimately responsible for any unpaid invoices.

- The factor may provide a higher advance rate compared to non-recourse factoring, but this comes with the added risk for the seller.

Credit: tritonstore.com.au

Exploring Non-recourse Factoring

Definition Of Non-recourse Factoring

Non-recourse factoring is a type of invoice financing where the factor assumes most of the risk of non-payment by your customers. In this arrangement, the factoring company takes on the responsibility for any non-payment of the invoices it purchases, minimizing the seller’s risk exposure.

Advantages And Disadvantages For The Seller

Advantages:

- Reduced risk: As the factor assumes the responsibility for non-payment, the seller is protected from potential losses due to customer default.

- Predictable cash flow: Sellers can rely on a more stable cash flow since they are shielded from the impact of non-payment.

- Access to working capital: Non-recourse factoring provides immediate funds against accounts receivable, enabling sellers to meet their short-term financial needs.

Disadvantages:

- Higher fees: Non-recourse factoring often involves higher fees compared to recourse factoring, as the factor assumes a greater risk.

- Stringent credit requirements: Factors may impose stricter credit criteria on the seller’s customers, which could limit the number of invoices eligible for non-recourse factoring.

- Limited control: Since the factor takes on the credit risk, they may exert more control over the collection process, potentially impacting the seller’s customer relationships.

Comparison: Domestic Factoring Vs. Export Factoring

Factoring, a widely-used financial practice, offers various types to cater to different business requirements. Two significant types are domestic factoring and export factoring. Understanding their differences and considerations is crucial for businesses engaged in domestic and international trade.

Definition Of Domestic Factoring

Domestic factoring is a financial arrangement in which a business sells its accounts receivable to a factor within the same country in order to improve cash flow and liquidity. The factor then takes over the responsibility of collecting the outstanding invoices.

Definition Of Export Factoring

Export factoring, on the other hand, involves the sale of accounts receivable to a factor when a business deals with international customers. The factor may provide services such as credit protection, financing, and collection of receivables across different countries.

Differences And Considerations

There are several differences and considerations when comparing domestic factoring to export factoring. One of the key distinctions is the geographical scope, where domestic factoring is limited to a single country, while export factoring involves cross-border trade. Export factoring may also provide additional services such as foreign currency exchange and credit protection due to the complexities involved in international transactions.

Credit: altline.sobanco.com

Frequently Asked Questions On Factoring And Types Of Factoring

What Is The Definition Of Factoring?

Factoring is when a business sells its accounts receivable (invoices) to a third party to meet short-term liquidity needs. The factor pays the invoice amount minus their commission or fees. There are different types of factoring, including recourse and non-recourse factoring.

What Are The 2 Types Of Invoice Factoring?

There are two types of invoice factoring: recourse and non-recourse factoring. Recourse factoring requires the selling company to buy back any unpaid invoices, while non-recourse factoring shifts the risk of non-payment to the factoring company. These types differ in fees, qualification requirements, and responsibility for nonpayment.

What Is Factoring With An Example?

Factoring is when a business sells its invoices to a third party to get immediate funds. For example, if a business sells $10,000 in invoices to a factor, they might receive $9,500 upfront and the remaining ($500) minus fees once the invoices are paid.

What Is Recourse And Nonrecourse Factoring?

Recourse factoring means the business is responsible for unpaid invoices. Non-recourse factoring shifts the risk to the factor.

Conclusion

Factoring is a versatile financing option for businesses looking to maintain a steady cash flow. This type of finance involves selling accounts receivable to a third party in exchange for immediate cash, minus a fee. There are several types of factoring, including recourse, non-recourse, domestic, export, disclosed, undisclosed, advance, and maturity factoring.

Understanding the different types of factoring can help businesses make informed decisions about their financial needs. By utilizing factoring, businesses can improve their liquidity and focus on growth and development.