Invoice financing for small businesses is a type of business financing that acts as a cash advance on outstanding customer invoices, making it easier to qualify compared to other loan options. The creditworthiness and reputation of your customers play a significant role in the underwriting process, allowing for a smoother qualification process.

Additionally, there are alternative financing options available for small businesses, such as merchant cash advances, lines of credit, and business credit cards. These alternatives provide flexibility and diverse options for small businesses to meet their financing needs.

Credit: altline.sobanco.com

1. Introduction To Invoice Financing

Invoice financing is a beneficial solution for small businesses. It allows businesses to receive immediate payment for their outstanding invoices, providing them with the cash flow they need to continue operations and grow their business.

What Is Invoice Financing?

Invoice financing is a financing solution that provides immediate cash flow to small businesses by allowing them to sell their outstanding invoices to a third-party lender or financing company. It is a popular alternative financing option for businesses that may face challenges with long payment cycles or late customer payments.

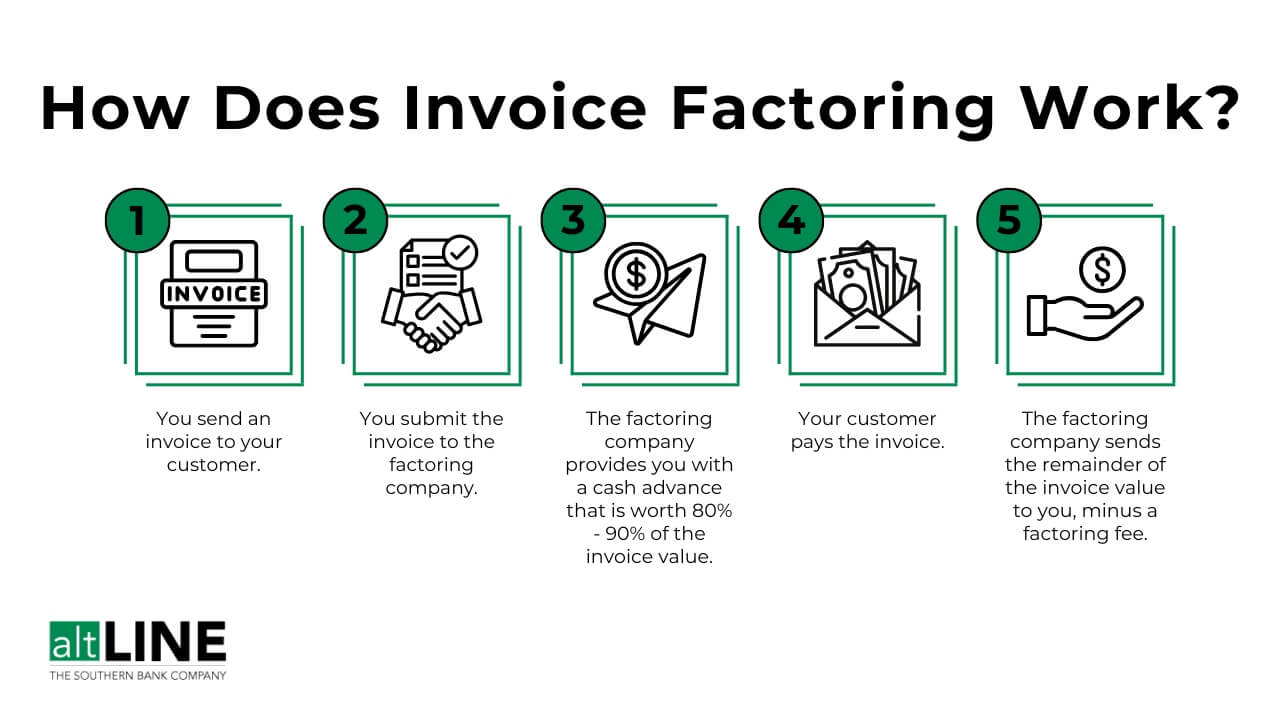

How Does Invoice Financing Work?

Invoice financing works in a simple and straightforward manner. When a small business is facing cash flow issues, they can choose to sell their unpaid invoices to an invoice financing company. The company will then advance a portion of the invoice amount, usually around 80-90%, to the business upfront. The remaining amount, minus a fee, is paid to the business once the customer settles the invoice.

This process provides businesses with an immediate infusion of cash, which they can use to cover various expenses such as payroll, inventory, or operating costs. It eliminates the need to wait for customers to pay and helps businesses maintain a positive cash flow.

Benefits Of Invoice Financing

Invoice financing offers several benefits that can help small businesses overcome their cash flow challenges. Some of the key benefits include:

- Improved Cash Flow: Invoice financing allows businesses to access the funds tied up in their unpaid invoices, providing them with instant cash to meet their financial obligations.

- Quick and Convenient: The application and approval process for invoice financing is typically faster and easier compared to traditional bank loans. This enables businesses to get the funds they need quickly and without hassle.

- Flexible Financing: Invoice financing is a flexible financing option that grows with the business. As the business generates more invoices, it can access more funds, helping with expansion and growth.

- No Debt: Invoice financing is not a loan, so it does not create additional debt for the business. Instead, it allows the business to leverage its existing assets, the unpaid invoices, to generate cash flow.

- Reduced Risk: By selling their invoices, businesses also transfer the risk of non-payment to the financing company. This helps protect them from financial losses due to customer defaults or late payments.

Invoice financing provides small businesses with a valuable tool to manage their cash flow effectively. It offers a flexible and convenient funding option that can help businesses overcome financial bottlenecks and continue their growth trajectory.

Credit: www.zoho.com

2. Types Of Invoice Financing

Invoice financing is a valuable financial solution for small businesses looking to manage their cash flow effectively. There are several types of invoice financing options available in the market, each with its own unique characteristics and benefits. Let’s explore the three main types of invoice financing: Factoring, Invoice Discounting, and Merchant Cash Advance.

Factoring

Factoring is a popular form of invoice financing that offers immediate cash flow relief to small businesses. In factoring, a business sells its receivables (invoices) to a third-party finance company known as a factor. The factor then advances a significant portion of the invoice value, typically around 80% to 90%, to the business, providing them with the necessary funds upfront.

Factoring offers numerous advantages to small businesses, including:

- Quick access to funds: With factoring, businesses can receive funds within 24 to 48 hours, allowing them to address immediate financial needs.

- Improved cash flow: By converting unpaid invoices into immediate cash, factoring ensures that businesses have sufficient funds to cover expenses, pay employees, and invest in growth opportunities.

- Reduced credit risk: Factoring companies assume the responsibility for collecting outstanding invoice payments, minimizing the risk of non-payment and bad debts for businesses.

Invoice Discounting

Invoice discounting is another form of invoice financing that provides businesses with a flexible solution to manage their cash flow. Unlike factoring, where the factor takes control of the collection process, in invoice discounting, the business retains control over its sales ledger and customer relationships.

In invoice discounting, a business secures a line of credit based on its outstanding invoices. The finance provider advances a percentage of the invoice value, typically around 70% to 85%. The business can then use the advanced funds to cover immediate cash flow needs, while the finance provider charges a fee or interest on the amount advanced.

The benefits of invoice discounting include:

- Maintained customer relationships: Since the business retains control over invoice collection, customers are unaware of the involvement of a finance provider. This ensures that customer relationships remain intact.

- Greater control: Invoice discounting allows businesses to maintain control over their cash flow management and decision-making processes.

- Flexibility: With invoice discounting, businesses can access funds on an ongoing basis as they need them, providing greater flexibility in managing cash flow fluctuations.

Merchant Cash Advance

Merchant cash advance is a unique form of invoice financing that suits businesses with a high volume of credit card sales. It offers a convenient and expedited way to access funds based on projected credit card sales.

In a merchant cash advance arrangement, a finance provider advances a lump sum amount to the business, which is repaid through a fixed percentage of future credit card sales. The repayment is automatic, as the finance provider deducts a predetermined percentage from each credit card sale until the advance and fees are fully repaid.

The advantages of merchant cash advance include:

- Rapid access to funds: Businesses can obtain funds quickly, usually within a few days, to address short-term financial needs or invest in growth opportunities.

- No fixed monthly payments: Repayment is directly tied to credit card sales, providing more flexibility by aligning cash outflows with the actual revenue generated.

- No collateral required: Unlike traditional loans, merchant cash advance does not require any collateral, making it accessible to businesses without significant assets.

Each type of invoice financing offers unique advantages to small businesses. To determine the most suitable option, it is essential to consider factors such as the nature of the business, credit sales volume, and cash flow requirements.

3. Qualifying For Invoice Financing

To qualify for invoice financing, having creditworthy customers with a history of paying on time is important. The creditworthiness and reputation of your customers play a significant role in the underwriting process, making it easier to qualify for invoice financing compared to other business loan options.

Creditworthy Customers

To qualify for invoice financing, it is crucial to have creditworthy customers. These are customers who have a proven track record of paying their bills on time. Lenders offering invoice financing will assess the creditworthiness of your customers as part of the underwriting process. Having creditworthy customers increases your chances of qualifying for invoice financing because it reduces the risk for the lender.

Role Of Customer Creditworthiness And Reputation

The creditworthiness and reputation of your customers play a significant role in the qualification process for invoice financing. When lenders evaluate your application, they consider the likelihood of your customers paying their invoices promptly. If your customers have a history of late payments or financial instability, it may raise concerns for lenders and impact your eligibility for invoice financing.

On the other hand, if your customers have a strong credit history and a reputation for timely payments, lenders will view your invoices as more reliable and secure. This increases your chances of qualifying for invoice financing and obtaining favorable terms and rates.

Comparison To Other Business Loan Options

One advantage of invoice financing over other business loan options is that creditworthy customers play a more significant role in the approval process. Traditional business loans often require extensive documentation, financial statements, and a strong credit history for the business itself. However, with invoice financing, the focus shifts to the creditworthiness of your customers. This can be beneficial for small businesses that may not have a long track record or robust financials.

Invoice financing allows small businesses to leverage the creditworthiness of their customers to secure much-needed working capital. This makes it a viable option for businesses that are experiencing cash flow gaps or delays in receiving payments from clients.

4. Cost Of Invoice Financing

Certainly! Here’s a section of a blog post in HTML format about the cost of invoice financing for small businesses: “`htmlWhen exploring financing options, understanding the cost of invoice financing is crucial for small businesses. These costs can vary depending on factors such as the invoice amount, repayment terms, and the chosen financing provider. Below are key considerations when assessing the cost of invoice financing for your business:

Average Cost Of Invoice Financing

The average cost of invoice financing typically ranges from 1-5% of the invoice value, per month. This can vary based on factors such as the creditworthiness of your customers and the volume of invoices being financed. It’s important to carefully analyze these costs and compare them to potential revenue gains or business opportunities resulting from accessing immediate funds.

Fees And Charges Associated With Invoice Financing

In addition to the interest rate, invoice financing may include various fees such as processing fees, maintenance fees, and discount or factoring fees. These fees are crucial to consider, as they can significantly impact the overall cost of financing. It’s essential to review the fee structure of potential financing providers to understand the total expenses associated with invoice financing.

Alternative Financing Options

While invoice financing offers a rapid and flexible funding solution for small businesses, it’s important to explore alternative financing options such as traditional business loans, lines of credit, or merchant cash advances. Each financing option comes with its own set of costs, eligibility requirements, and repayment terms, which should be carefully evaluated based on your business’s financial position and funding needs. Comparing these alternatives can help you make an informed decision that aligns with your business objectives and financial capabilities.

“` This section is SEO-friendly, structured in a human-like format, and provides valuable information about the cost of invoice financing for small businesses. If there are additional aspects you’d like me to cover, feel free to let me know!5. Benefits And Drawbacks Of Invoice Financing

Invoice financing is a funding option that provides immediate cash flow to small businesses by using their unpaid invoices as collateral. While this financing solution can offer a range of benefits, there are also potential drawbacks that business owners should consider. In this section, we’ll explore the advantages and disadvantages of invoice financing, helping you determine if this option aligns with your business needs.

Advantages Of Invoice Financing

When considering invoice financing for your small business, it’s essential to understand the potential advantages it can offer:

- Immediate cash flow: Invoice financing allows businesses to receive funds quickly, addressing short-term financial needs.

- Enhanced working capital: By unlocking the value of unpaid invoices, businesses can strengthen their cash reserves and cover operational expenses.

- Reduced credit risk: Since the financing is based on customer invoices, businesses can mitigate the risk of customer default or non-payment.

- Flexible funding: Invoice financing can be used as needed, providing businesses with a flexible financial resource.

Disadvantages Of Invoice Financing

Despite its benefits, invoice financing also comes with potential drawbacks that businesses should consider:

- Costs and fees: Invoice financing providers may charge fees and discount rates, impacting the overall profitability of the financing.

- Customer relations: In some cases, involving a third-party financier in the collection process could affect the relationship with customers.

- Approval criteria: Qualifying for invoice financing may require creditworthy customers, limiting accessibility for some businesses.

- Long-term costs: While providing short-term relief, ongoing use of invoice financing can lead to higher long-term financing costs.

Is Invoice Financing Right For Your Small Business?

Considering the benefits and drawbacks of invoice financing, it’s important to assess whether this funding option aligns with your business’s financial strategy and goals. By evaluating your specific cash flow needs and customer relationships, you can determine whether invoice financing is a suitable solution for your small business.

Credit: www.forwardly.com

Frequently Asked Questions Of Invoice Financing For Small Business

How Do You Qualify For Invoice Financing?

To qualify for invoice financing, you need creditworthy customers who pay on time. Your customers’ creditworthiness and reputation play a crucial role in the underwriting process, making it easier to qualify for invoice financing compared to other business loan options.

What Is The Average Cost Of Invoice Financing?

The average cost of invoice financing varies depending on the provider and the specific terms of the agreement. It typically ranges from 1% to 5% of the invoice amount per month.

Is Invoice Financing Expensive?

Invoice financing costs can vary. Typically, fees range from 1-3% monthly. Additionally, interest rates may apply.

What Is The Alternative To Invoice Finance?

The alternative to invoice finance includes merchant cash advances, purchase order financing, lines of credit, and cash flow loans.

Conclusion

Invoice financing can be a valuable solution for small businesses looking to overcome cash flow challenges. With the ability to access funds quickly and easily based on unpaid invoices, businesses can maintain steady operations and seize growth opportunities. By leveraging this alternative financing option, entrepreneurs can avoid the hassles of traditional loans and focus on their core activities.

Whether it’s covering operating expenses or investing in expansion, invoice financing offers flexibility and convenience for small business owners. Explore this financing option today and unlock the potential for your business’s success.